Stablecoin Due Diligence: The Essential Guide to Risks and Types

Navigating the Complex World of Stablecoin Finance

Stablecoins promise a simple idea: the ease of cryptocurrency with the steady value of traditional money. They are digital currencies designed to keep a stable value, often by being pegged to an asset like the US dollar. It sounds perfect for managing digital cash, sending fast payments, or exploring other parts of the crypto world.

But here’s the thing. That promise of stability is wrapped in layers of technical complexity. This creates a huge barrier for anyone trying to use them wisely.

You don’t just choose a "stablecoin." You’re choosing between fundamentally different designs, each with its own risks and rules.

According to industry experts, the main types are fiat-backed, crypto-collateralized, and algorithmic models, which all work in very different ways.

This isn’t just academic. The financial risk of picking the wrong one is real and can be substantial. Some stablecoins are backed by real cash reserves in a bank. Others use complex algorithms or are backed by other, more volatile cryptocurrencies. If trust in that system fails, it can trigger a "run" and cause the stablecoin to lose its peg, an event that major financial institutions warn can destabilize the broader ecosystem. History has shown us painful examples of what happens when these systems fail.

For individuals and business owners, this is a minefield. How can you tell if a stablecoin’s reserves are truly safe and transparent? What’s the difference between a "collateralized" and an "algorithmic" coin? Reliable, clear guidance that cuts through the hype and technical jargon is surprisingly scarce. This makes it incredibly difficult to make informed, confident decisions about your digital assets.

You don’t have to navigate this alone. Getting clear, step-by-step education is the best first move. For straightforward explanations on topics like this sent directly to you, consider subscribing to the free Clicks and Trades newsletter. It breaks down crypto concepts into plain language, helping you build knowledge safely.

Ready to start understanding stablecoins with confidence? Sign Up for free guidance today.

Beyond the Buzzword: What Are Stablecoins Really?

You hear the term "stablecoin" a lot. It sounds simple, like a calm version of Bitcoin. But what does it actually mean? And why should you care?

Think of a stablecoin as a digital token that tries to be as stable as a dollar in your bank account. Its main job is to fight the wild price swings of other cryptocurrencies. This stability is the key that unlocks real-world uses, like sending instant payments or keeping savings in the digital world without watching the value jump up and down every hour.

But here’s the crucial part. Not all stablecoins are built the same way. Saying you use a stablecoin is like saying you drive a car. It doesn’t tell you if it’s an electric sedan, a diesel truck, or a experimental vehicle with no engine. The "how" matters more than the "what."

Experts break stablecoins into three main types based on what backs them up, or their collateral. Understanding this is the first step to using them wisely.

The Three Main Types of Stablecoins

-

Fiat-Collateralized (Like a Digital IOU): This is the most common type. For every digital coin that exists, a company holds one real US dollar (or euro, etc.) in a bank. It’s a simple promise: you can always trade your coin back for the cash. Major financial advisors note these are digital assets that maintain financial reserves in fiat currency held by a regulated institution such as a bank.

-

Crypto-Collateralized (Backed by Other Crypto): Instead of dollars in a bank, these stablecoins are backed by a reserve of other cryptocurrencies, like Ethereum. To account for the reserve crypto’s volatility, the system often holds more crypto than the value of the stablecoins issued. It’s a more complex, decentralized model.

-

Algorithmic (The Rule-Based Model): These have no physical cash or simple crypto reserve. Instead, they use smart contracts and computer algorithms to automatically control the supply of coins, aiming to keep the price stable. The Federal Reserve describes these as aiming to maintain exchange rate stability by employing a set of rules and algorithms. They are often seen as the most innovative but also the riskiest design.

Why "Stable" Matters for You

This isn’t just tech talk. The promise of stability is what makes stablecoins useful for everyday things. They aim to be a bridge between traditional money and the crypto world. You can use them to:

- Send money across borders quickly and cheaply.

- Earn interest on your digital savings.

- Easily trade in and out of other cryptocurrencies without going back to your bank.

However, this promise depends entirely on the people and systems behind the coin. You have issuers (the companies that create them), custodians (who hold the reserves), auditors (who check the reserves), and the blockchain networks they run on. Trust in this whole chain is what keeps the coin stable.

Getting a handle on these basics is a powerful first step. It moves you beyond just hearing the buzzword to understanding the machinery. This knowledge is more practical for your digital cash than searching for general terms like "Exeter Finance" or "regional finance." It’s about the new rules of digital money.

For clear, step-by-step guides that break down topics like this into plain language, subscribing to a free educational resource can help. The Clicks and Trades newsletter offers straightforward explanations to help you build your crypto knowledge safely and confidently.

Ready to move past the jargon and understand how to evaluate these tools for yourself? Sign Up for free guidance and take control of your financial learning today.

The Core Challenges: Why Stablecoin Due Diligence is Non-Negotiable

Now you know the different types of stablecoins. But here’s the real question. How do you know you can trust them?

The promise of stability is not a guarantee. It’s a goal held together by technology, people, and rules that can sometimes fail. Doing your homework, what experts call "due diligence," isn’t just smart. It’s essential for protecting your money.

This is more critical than simply comparing traditional lenders or looking up general terms like "Exeter Finance" or "regional finance." You’re dealing with a new kind of digital cash with its own unique risks.

Let’s break down the core challenges you need to understand.

Specific Risks by Stablecoin Type

Each type of stablecoin we discussed has a different Achilles’ heel.

- Fiat-Collateralized: The Risk of Bank Failure. Your stablecoin is only as safe as the bank holding the cash. If the issuer’s banking partner fails or faces problems, your "digital dollar" might not be redeemable for a real dollar. The promise depends entirely on that third-party institution.

- Crypto-Collateralized: Volatility Cascades. These coins are backed by other cryptocurrencies, which are famously unstable. If the value of the reserve crypto crashes suddenly, the system might not have enough value to back all the stablecoins. This can force rapid sales of the reserve, crashing its price further in a dangerous spiral. A report from late 2025 noted that the stablecoin sector remains exposed to such interconnected risks.

- Algorithmic: The "Death Spiral." This is the riskiest design. Algorithmic coins have no cash reserve. They rely on complex code and market incentives to hold their value. If people lose faith and start selling, the system is designed to create more coins to push the price back up. But if panic is too great, this can fail catastrophically. The system collapses as the coin’s value falls toward zero. The 2022 collapse of UST, which wiped out over $40 billion, is the classic example of this failure mode.

The Big Problem: Reserve Opacity

This phrase means "you can’t see what’s backing the coin." It’s a major issue.

You might hear a stablecoin is "fully backed," but what does that mean? Are the reserves all cash in a top-tier bank? Or are they commercial paper, treasury bonds, or even loans to other crypto companies?

The problem is that not all issuers provide clear, frequent, and verified proof of their reserves. Historical examples show that some have misrepresented their holdings. This lack of transparency means you could think you own a digital dollar, but you actually own a digital IOU for a risky asset. When trust evaporates, it can trigger a run on the stablecoin and cause it to lose its peg to the dollar, as noted by the European Central Bank.

A Shifting Regulatory Landscape

Rules for stablecoins are changing fast and vary wildly by where you live. This is a dynamic risk factor.

- Some places are creating clear rules. For instance, the UK’s Financial Conduct Authority (FCA) is proposing new regulations for stablecoin issuance, which aims to enhance consumer protection.

- Other regions have different approaches. The European Union has its comprehensive Markets in Crypto-Assets (MiCA) framework, while other countries may ban or restrict their use entirely.

Why does this matter to you? If you use a stablecoin issued in a country with weak regulations, you may have little recourse if something goes wrong. If you live in a place that suddenly restricts stablecoins, accessing your funds could become difficult. Navigating this patchwork of rules is part of the due diligence process.

The bottom line is simple. Using stablecoins without understanding these risks is like driving with your eyes closed. The stability is appealing, but the foundations need inspection.

Getting clear, unbiased information is the first step to safety. For ongoing guidance that helps you understand these complex topics, consider subscribing to a free educational resource like the Clicks and Trades newsletter. It offers straightforward explanations to help you build your knowledge confidently.

Don’t leave your digital cash to chance. Sign Up for free today and learn how to evaluate stablecoins with a critical, informed eye.

A Framework for Trust and Transparency: What to Look For

So you know the risks. The question now is, how do you spot a good stablecoin? The goal isn’t just to find a coin that works today. It’s to find one built on a foundation of trust that will last. This goes far beyond a simple web search like "finance Google" or trusting a name because it sounds established, like "regional finance" or "American Honda Finance."

You need a clear framework. Think of it like inspecting a house before you buy it. You check the foundation, the roof, and the plumbing. For a stablecoin, you check three critical things: its reserves, the proof backing it, and its redemption policy.

The Three Pillars of a Reliable Stablecoin

A trustworthy stablecoin stands on three pillars. If one is weak, the whole structure is risky.

-

Verifiable Reserves: This is the "what." A reliable issuer tells you exactly what assets are in the vault backing the coins. Are they all U.S. dollars in a bank? A mix of cash and short-term U.S. Treasury bills? The specific breakdown matters because not all assets are equally safe or easy to sell. Look for a detailed, itemized list of reserve assets.

-

Regular Attestations and Audits: The "Proof." This is how you verify the "what." An attestation is a report where an independent accounting firm checks the issuer’s numbers at a point in time and says, "Yes, the reserves matched the liabilities on this date." A full audit is more rigorous, examining internal controls and processes over a period.

- Why does this matter? New rules like the GENIUS Act of 2025 are making monthly attestations mandatory for major issuers. This push for transparency is powered by professional standards. For example, the American Institute of CPAs (AICPA) has created comprehensive reporting criteria for stablecoins to ensure consistency and clarity. In 2026, leading accounting firms use these standards to build trust in stablecoin reporting. Always check for recent, independent reports.

-

Clear Redemption Policy: The "How." Can you actually get your money out? A clear policy explains the steps to redeem your stablecoins for the underlying asset (like U.S. dollars). How long does it take? Are there fees? If this process is slow, complicated, or opaque, it’s a major red flag.

Your Issuer Credibility Checklist

The technology is important, but so are the people behind it. Before you trust a stablecoin, research the issuer.

- Team Background: Who runs the company? Look for experienced leaders with proven track records in finance, technology, or compliance.

- Governance Structure: How are decisions made? Is there a clear, responsible entity, or is it an anonymous group?

- Communication History: Read their official blogs and announcements. Do they communicate openly during both good and bad market times? Have they ever been misleading?

- Regulatory Standing: Are they licensed or registered with financial authorities in a major jurisdiction like the U.K. or parts of the U.S.? Operating in a regulatory gray area is a risk.

Do-It-Yourself Verification: On-Chain Analytics

Here’s the powerful part. You don’t have to take anyone’s word for it. You can verify much of the data yourself using blockchain explorers.

A blockchain explorer is like a public ledger viewer. You can look up any stablecoin’s contract address and see real-time data.

What you can check:

- Total Supply: How many tokens exist right now?

- Large Wallet Movements: Are big amounts being moved to or from exchanges?

- Transaction History: Is the network active?

While you can’t see the off-chain bank reserves here, you can verify the on-chain token supply. Some advanced services even aim to close the gap with real-time reserve reporting. By cross-referencing the issuer’s published attestation (e.g., "We hold $5B in reserves on June 1") with the on-chain supply on that same date, you can perform a basic sanity check.

Evaluating stablecoins takes a bit of work, but it’s the key to safe participation in crypto. For clear step-by-step guidance on this process, many find it helpful to follow a straightforward educational resource like the Clicks and Trades newsletter. It breaks down these concepts without the jargon, helping you build confidence.

Ready to look at stablecoins with a more informed eye? Sign Up for free insights and learn how to protect your digital cash.

Stablecoin Risk Assessment Matrix

Now you have a framework. The next step is to apply it. This matrix helps you compare some of the most well-known stablecoins. Think of it as a simplified scorecard.

It is not a final recommendation. It is a tool to start your own research.

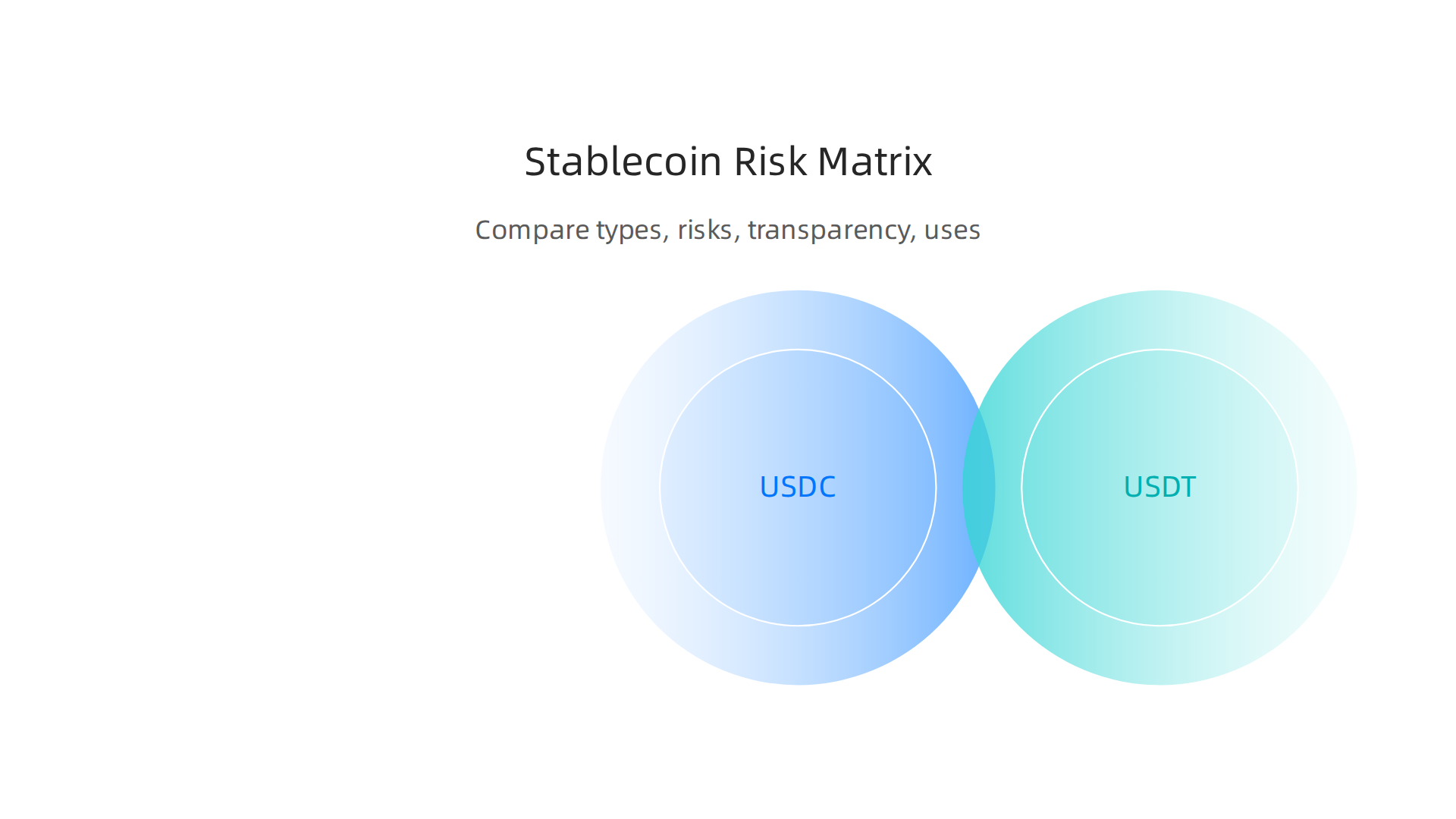

| Stablecoin | Type (Primary) | Key Risks to Consider | Transparency & Attestations (as of 2026) | Best For… |

|---|---|---|---|---|

| USDC | Fiat-Collateralized (Cash & Bonds) | Regulatory actions, banking partner risk. | High. Publishes monthly attestation reports by top accounting firms under the latest AICPA stablecoin reporting criteria. | Beginners and institutions wanting high trust and regulatory clarity. |

| USDT | Fiat-Collateralized (Mix of assets) | Reserve composition scrutiny, regulatory pressure. | Medium/Improving. Now provides quarterly attestations, moving toward the monthly standard required by laws like the GENIUS Act of 2025. | Advanced users comfortable with ongoing due diligence. |

| DAI | Crypto-Collateralized | Market volatility, smart contract risk, complexity. | High (for its type). Reserves are fully on-chain and verifiable in real-time. | Users who prioritize decentralization and understand DeFi risks. |

| Tether Gold | Commodity-Collateralized | Physical gold custody risk, lower liquidity. | Medium. Regular attestations confirm gold bars are audited and held, but verifying physical assets has unique challenges. | Investors seeking crypto exposure to a traditional asset like gold. |

| Algorithmic (various) | Algorithmic | Collapse of the peg if the algorithm fails, extreme volatility. | Typically Low. Many lack independent, standardized reserve reports, as they don’t hold traditional collateral. | Speculative, advanced users only. High risk. |

How to Use This Matrix

Do not just pick the one in the "Best For Beginners" row. Your choice depends on your own goals.

- Match the "Best For…" to your profile. Are you just moving cash between exchanges? A simple, high-transparency option might be best. Are you building in DeFi? You might accept different risks.

- Look at the "Key Risks." Ask yourself: Which of these risks am I comfortable with? If "regulatory risk" keeps you up at night, you’ll choose differently than someone focused on "smart contract risk."

- Verify the "Transparency" claim. This is where your framework kicks in. Go to the issuer’s website. Find their latest report. See if a major firm like PwC confirms it helps build trust in stablecoin reporting. This is your work, beyond a simple "finance Google" search.

- This is a snapshot. The world changes fast. A stablecoin with "Medium" transparency today could improve to "High" next month with a new audit. Or, it could face a new challenge.

Remember, this is about inspecting for yourself. It is very different from dealing with a traditional loan company like Exeter Finance or checking your local county website like the NYC Department of Finance. In crypto, you are your own chief inspector.

For ongoing, plain-English analysis that helps you keep up with these changes, consider following a free resource like the Clicks and Trades newsletter. It breaks down complex topics into simple steps.

Ready to take the next step in your crypto education with clear, trusted guidance? You can Sign Up for free.

Practical Use Cases: From Personal Finance to Business Operations

So you have a framework to assess risk. Great. Now, what can you actually do with a stablecoin? This isn’t just theory. In 2026, people and businesses are using them for real jobs that traditional finance often does slowly or expensively.

Think of it this way: you wouldn’t use a complex loan from a company like Exeter Finance to buy a cup of coffee. Different tools for different jobs. Stablecoins are a new financial tool. Let’s look at where they fit.

For Individuals: Managing Your Money

You can use stablecoins for more than just trading crypto. Here are three practical ways:

- Cheaper, Faster Cross-Border Remittances. Sending money home to family across borders can be slow and expensive with traditional wire transfers. Stablecoins can settle in minutes for a fraction of the cost.

By August 2025, stablecoin remittances hit a $19 billion annualized run rate, showing real adoption.

-

A Hedge Against Local Currency Inflation. If your local currency is losing value fast, holding a USD-pegged stablecoin can be a way to protect your purchasing power. It’s like having a digital dollar account, accessible from anywhere.

-

Earning Yield Through DeFi Protocols. Instead of letting cash sit idle, you can deposit certain stablecoins into decentralized finance (DeFi) platforms to earn interest. This is where the "crypto-collateralized" stablecoins like DAI often shine. Important: This comes with smart contract risk and complexity, as our risk matrix showed. The yield is a reward for taking on that additional risk.

For Small & Medium Businesses (SMBs): Streamlining Operations

This is where stablecoin use has exploded. Actual stablecoin payment volume for real economic activity reached $390 billion in 2025. For businesses, it’s about efficiency.

-

Treasury Management. A business can hold a portion of its working capital in a transparent, high-quality stablecoin. This can be quicker to deploy than traditional bank balances for certain needs, and in some cases, can earn a yield.

-

Faster, Cheaper International B2B Payments. This is the biggest use case today. McKinsey estimates that B2B stablecoin payments account for roughly $226 billion per year. Paying an international supplier can be as simple as sending a digital token, bypassing multi-day bank delays and high forex fees.

-

Paying Remote Contractors. Hiring talent globally? You can pay them instantly in a stable digital dollar, simplifying payroll across borders.

The Trade-Offs: Convenience, Yield, and Risk

Your choice always involves a balance. It’s not about finding the "best" stablecoin, but the right tool for your specific need.

- Prioritizing Convenience & Low Risk? For sending value quickly or holding working capital, a simple, highly-regulated stablecoin like USDC is often the best fit. You sacrifice potential yield for maximum stability and trust.

- Chasing Higher Yield? To earn interest in DeFi, you might use a decentralized stablecoin. You gain yield but must accept more complexity and smart contract risk.

- Making Large Business Transfers? Transparency is non-negotiable. You need the clear attestation reports we discussed earlier, not just a quick finance Google search. This due diligence is very different from checking a payment status with your local NYC Department of Finance or reviewing a statement from American Honda Finance. You are verifying the asset itself.

Align your choice with your goal. Sending rent money to a friend? Use the simplest option. Building a DeFi yield strategy? You’ll need to understand the deeper risks.

The landscape changes fast. For ongoing, plain-English analysis that helps you keep up with these practical uses and risks, follow a free resource like the Clicks and Trades newsletter. It breaks down complex topics into simple steps.

Ready to take the next step in your crypto education with clear, trusted guidance? You can Sign Up for free.

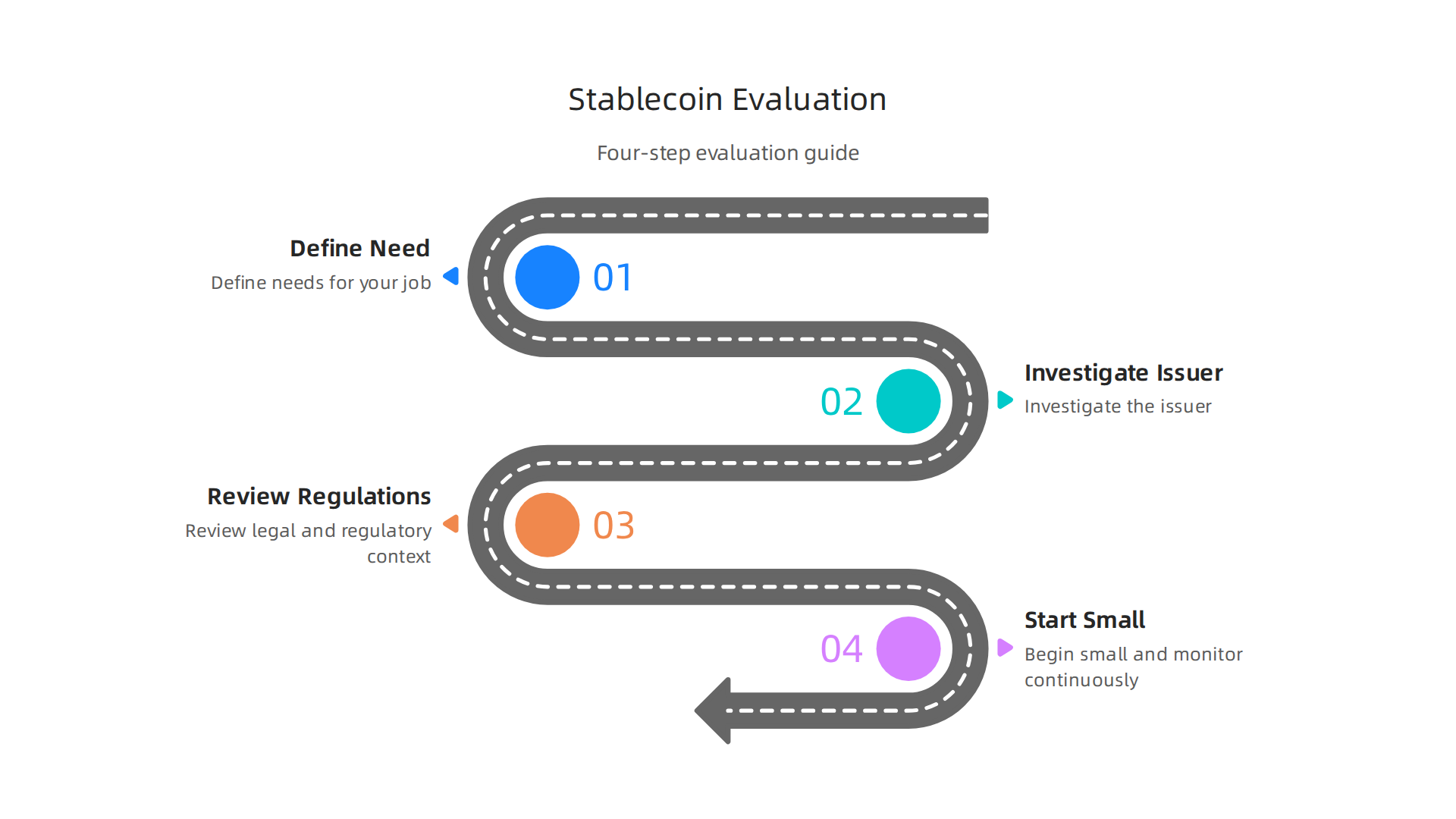

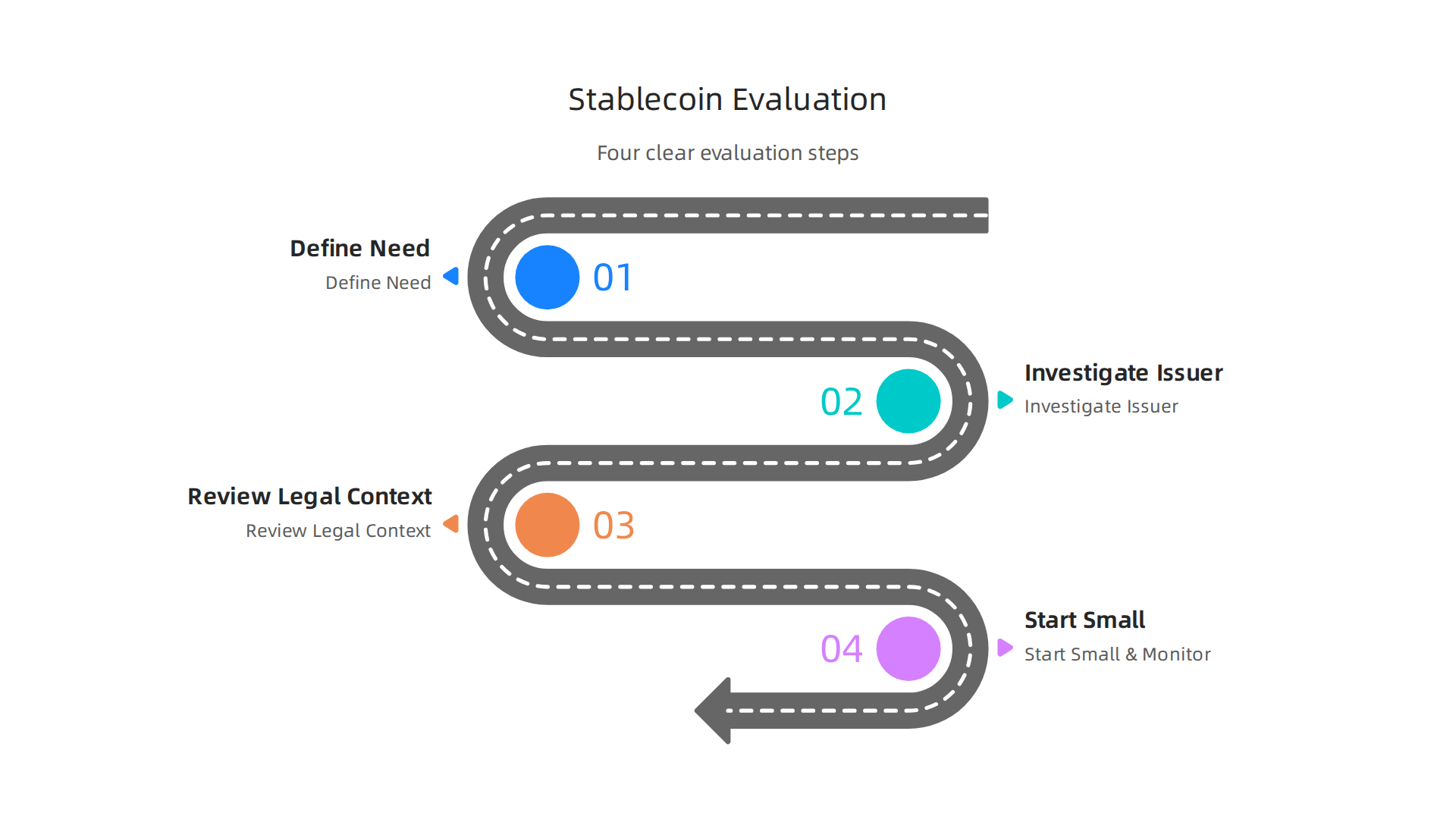

A Step-by-Step Guide to Evaluating a Stablecoin Service

Okay, you know what you can use a stablecoin for. Now, how do you pick one? This is where smart research, not guesses, matters most.

Your checklist for a stablecoin isn’t the same as for a traditional loan from a company like Exeter Finance, where you’d check credit terms. It’s also not a quick finance Google search for reviews. You’re not just verifying a business license with your local NYC Department of Finance.

You are investigating a digital asset. Your goal is to see if it’s a reliable tool for your specific job. Let’s break it down into four clear steps.

Step 1: Define Your Need and Risk Tolerance

Before you look at any coin, look in the mirror. Ask yourself: what is this for? Your answer determines everything.

- Is it for holding savings? Your priority is maximum safety and trust. You’ll want the simplest, most regulated option.

- Is it for sending money abroad once? You need low cost and speed. Extreme decentralization might be less important.

- Is it for earning yield in DeFi? You must accept higher complexity and smart contract risk for that potential reward.

This step aligns your choice with your goal. It stops you from using a risky, complex tool for a simple job. A general due diligence framework always starts by defining the asset’s purpose and your own risk appetite.

Step 2: Investigate the Issuer and Mechanics

Now, apply the transparency framework we discussed earlier. This is your deep dive.

- Who is the issuer? Are they a known, regulated entity like a trust company, or an anonymous decentralized autonomous organization (DAO)? Search for their official site, leadership team, and legal jurisdiction.

- What backs the coin? Go beyond the marketing. Look for the latest attestation report (for fiat-backed coins) or collateral dashboard (for crypto-backed coins). Are reserves held in cash and short-term bonds, or in riskier assets? High concentration in one asset is a red flag.

- How does it work? Understand the basic mechanics. Is it governed by a smart contract you can audit? If it’s algorithmic, what triggers the stability mechanism? Professional investors use a structured technology due diligence process to assess these digital systems, and you should adopt a simpler version.

Step 3: Review the Legal and Regulatory Context

This is about your rights. Where you live changes the rules.

- Is the issuer licensed where you are? A stablecoin regulated by New York’s Department of Financial Services (like some major ones) operates under strict rules. An offshore issuer may not.

- What happens if something goes wrong? Do you have any legal recourse? The terms of service matter here. This is different from dealing with a traditional lender like American Honda Finance or Republic Finance, where consumer protection laws are well-established.

- Is it compliant? Check recent news. Has the issuer faced any regulatory actions or lawsuits? Staying informed is key. Resources like the free Clicks and Trades newsletter often summarize major regulatory changes in plain language, helping you keep up.

Step 4: Start Small and Monitor

You’ve done your homework. Now, test the waters.

Never commit a large amount of money on your first try. Use a small, "can-afford-to-lose" amount for your initial transaction or holding period. This lets you:

- Test the actual user experience of sending and receiving.

- Verify the transaction speed and network fees.

- Build comfort before scaling up.

Your job isn’t over after you buy. Continuously monitor the health of the stablecoin. Sign up for issuer updates, watch for news on its reserves, and be aware of broader market conditions. Risk management in digital assets is an ongoing process, not a one-time check.

Following these steps moves you from hoping to knowing. It transforms a confusing array of options into a clear, informed decision. For ongoing guidance through this ever-changing landscape with clear, step-by-step advice, consider signing up for free insights.

Essential Tools and Resources for Ongoing Monitoring

You’ve done your initial research and made a choice. Great. But your job isn’t over. Think of it this way: you wouldn’t take out a car loan with Exeter Finance and then never check your statements or payment history. Managing a stablecoin requires the same ongoing awareness. Here are the essential tools to keep your finger on the pulse.

Your Digital Monitoring Toolkit:

- Blockchain Explorers: These are your live transaction trackers. Sites like Etherscan (for Ethereum) or BscScan (for BNB Chain) let you see every move of your stablecoin in real time.

You can verify transactions, check wallet balances, and confirm everything is working as it should.

- On-Chain Analytics Platforms: For a deeper health check, platforms like DeFi Llama or Dune Analytics show the big picture.

You can see the total value locked in a stablecoin’s protocol, monitor reserve compositions, and track adoption trends. This goes beyond finance basics into real-time data.

- Regulatory News Aggregators: Rules change fast. Don’t rely on a casual finance Google search. Follow dedicated crypto law blogs or set Google News alerts for your stablecoin’s issuer and key terms like “stablecoin regulation.”

- Official Community Forums: Go to the source. Many projects have governance forums where changes are discussed. This is where you learn about upcoming votes on fees, collateral types, or other critical updates.

Set Up Your Alerts:

Don’t wait for news to find you. Proactively set up alerts for:

- New audit or attestation reports from the issuer.

- Major governance proposals or votes.

- Mentions of the issuer in major financial news outlets.

A Crucial Warning:

Your financial safety depends on reliable information. Avoid relying solely on social media hype or unverified influencers for critical decisions. A structured due diligence checklist is a better guide than random online chatter. True risk management means using trustworthy sources.

Staying informed doesn’t have to be a full-time job. For a curated, easy-to-understand digest of the changes that matter, consider the free Clicks and Trades newsletter. It delivers step-by-step guidance and safety tips straight to your inbox. Sign Up for free to make ongoing monitoring simple.

The Future of Stablecoins and Navigational Services

Think back to that Exeter Finance car loan. You wouldn’t just check your statements once and forget about it for five years. The terms, the rates, the rules they operate under can all change. The world of stablecoins is the same, but the changes are happening at lightning speed.

As we look ahead, the landscape is shifting from a wild frontier to a more structured financial system. The tools and rules are evolving.

Here are the key trends that will define your experience in 2026 and beyond.

1. Clear Rules Are Coming (Finally)

For years, stablecoins operated in a gray area. That’s changing fast. Governments worldwide are crafting specific rules for how stablecoins should be issued, backed, and disclosed. This push for regulatory clarity, as noted in major industry outlooks, aims to protect users and bring stability to the market. It means you’ll have better, legally required information to work with, moving the entire sector beyond finance basics into a more secure era.

2. New Players and Models

Two big developments are on the horizon:

- Central Bank Digital Currencies (CBDCs): Countries are exploring their own digital cash. While different from decentralized stablecoins, their arrival will change how we all think about digital money.

- Institutional-Grade Issuance: Expect to see more stablecoins launched by large, regulated financial institutions. These aim to offer the trust of traditional regional finance with the efficiency of blockchain. As BlackRock highlighted in its 2026 outlook, this trend could significantly challenge traditional monetary systems.

3. Smarter, More Private Technology

The tools for verifying stability are getting a major upgrade. A key innovation is zero-knowledge proofs. Think of it this way: this technology allows a stablecoin issuer to cryptographically prove their reserves are fully backed without revealing every single private transaction detail. It’s a potential win-win for both verifiable trust and personal privacy. Experts point to such advances as key trends for making stablecoins more robust and user-friendly.

The One Thing That Won’t Change

No matter how fancy the technology gets or how clear the NYC Department of Finance posts its new guidelines, your most important habit remains the same: due diligence. The core principles of seeking transparency, verifying claims, and understanding what backs your digital dollar are permanent. Your financial safety will always depend on your willingness to look under the hood.

The future is promising, but it requires an informed navigator. Staying updated on these shifts doesn’t have to be confusing. For a clear, step-by-step breakdown of what these changes mean for you, consider the free Clicks and Trades newsletter. It turns complex trends into actionable guidance. Sign Up for free to make sure you’re always navigating with a reliable map.

Summary

Stablecoins aim to combine crypto convenience with fiat stability, but their designs and risks vary widely. This article explains the three main types—fiat-collateralized, crypto-collateralized, and algorithmic—and why those differences matter for safety, liquidity, and real-world use. It walks through the core challenges, including reserve opacity, bank and market risk, and shifting regulation, and offers a clear framework built on verifiable reserves, regular attestations/audits, and a transparent redemption policy. You’ll get a practical four-step evaluation process (define your need, inspect the issuer, review legal context, start small), a comparison matrix of common stablecoins, and real use cases for individuals and businesses. The guide also lists monitoring tools (blockchain explorers, analytics platforms, regulatory trackers) and explains how to set alerts and manage ongoing risk. After reading, you’ll know how to ask the right questions, perform basic on-chain checks, and choose a stablecoin that fits your purpose and risk tolerance.